Perhaps the most important thing to know about finance is what are the unintended consequences of a proposed course of action. Unfortunately, these are very rarely discussed. What is discussed, rather, are over-simplified, numerical projections often with faulty inputs to boot. Then, armed with this false information, the consumer draws erroneous conclusions…often with devastating results. All the while the financial services industry stands by, profiting from the darkened minds of the buying public rather than correcting the faulty notions of their clients.

Now I don’t want to join in the chorus of offering over-simplified or faulty projections. And I have already written on this blog my disdain for the typical “rate of return” discussion. Finance is more complex than that. However, to prove my earlier assertions, I do think it will be helpful to make a comparison of two oft-debated courses of action for paying off one’s home. I believe it will be illustrative of both the poor method by which courses of action are proposed and analyzed as well as offer an insight into how real world finance and unintended consequences are the more important issues in making these type decisions. So please pardon my use of numbers and projections. I promise to keep them simple, accurate and easily verifiable if you choose to do so.

So first let’s state the issue: Which is better a 30-year mortgage or a 15-year mortgage? The widely held belief (at least by the number of people I encounter holding it) is this: If you can afford it, a 15-year is better because you will have a lower interest rate, pay less in interest and get out of debt quicker. All the answers are true, as far as they go, but not dispositive of the issue especially as it pertains to real world finance. So let’s examine the facts in greater detail.

Anyone can go to bankrate.com and find the national averages for 15 and 30 year mortgages and quickly establish that the 15-year rates are better. As of today, 2.91% for the 15-year term and 3.66% for the 30-year term. Score “1” for the 15-year mortgage!

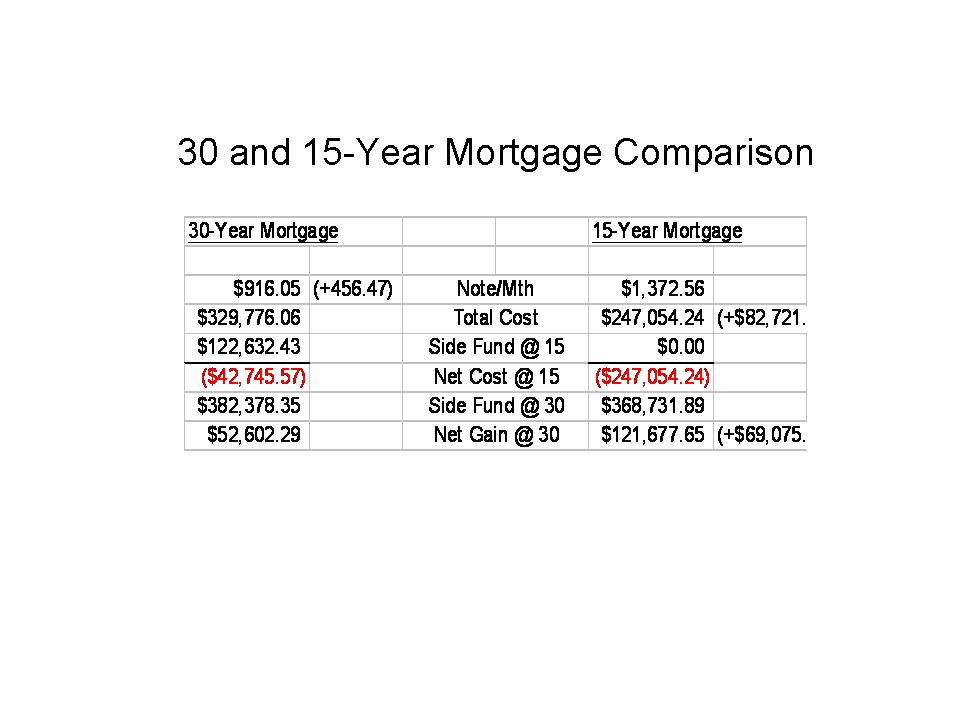

Similarly, it is quite easy to run two amortization schedules and see that indeed, less interest in paid on the 15-year mortgage. I ran an imaginary $200,000 loan and found that the 15-year mortgage at 2.91% interest would result in a total cost of $247,054.24, while the 30-year loan at 3.66% interest would result in a total cost of $329,776.06. Clearly, $47,054.24 in interest is lower than $129,776.06. Score another one for the short-term loan.

Ordinarily, this is where the analysis stops…and hence the faulty conclusion drawn. Add to this the “fact” that you will get out of debt 15 years faster and the case is a slam dunk. Or is it?

Not if we take a look at what actually happens to the person who takes this 15-year mortgage. Remember the conditional statement that prefaced the argument in favor of a 15-year mortgage: “If you can afford it….” In fact, the short-term mortgagee is paying a note 49.8% higher than the 30-year borrower, $1,372.52 versus $916.05. This is a $456.47 per month increase.

But that is not a problem since we assumed the person could pay the higher note. The real question rather is: Who is more likely to have additional resources to save and invest? If we assume that these people are of equal means (and we will assume this or the comparison will have no value), then clearly the longer term mortgagee is MORE likely to save money. This is real world issue number one: People have limited resources and must make the resources stretch to cover multiple items.

So, let’s assume that the 30-year borrower does indeed save some money, the $456.47 per month that he is not paying in mortgage expenses. And let’s assume he does this for 15 years at 5%. How are the two borrowers positioned now?

Well, the 15-year mortgagee just got out of debt by spending $247,054.24. Let’s hope he never hit any bumps in the road and never needed cash along the way since all of his available money was going to pay off debt…and he wouldn’t want to incur any others!

But the 30-year mortgagee over that same time frame would have accumulated $122,632.43. Yes, he would still be in debt, but throughout the first 15 years of the mortgage he would have had money available for any issue that arose as compared to his counterpart who would not have. This is a big deal in the real world because it will keep you from getting into a cycle of debt. That is why I advocate “becoming your own banker”, but I digress.

At this point, if we compare net costs, the short term borrower is out $247,054.24, the total cost of the loan, while the long term borrower is out $42,256.57 in net costs (this total is derived from taking his total payments over 15 years, $164,889, and subtracting his accumulated side fund, $122,632.43, but we must recall that he still has outstanding debt which we will address in a moment).

But now we are starting to see the unintended consequences and real world dilemmas and why they are so important. In fact, if we revised the mortgage question to more accurately depict the likely outcome of the arrangements, then the “better” of the two choices begins to shift. For example, if I proposed to you:

Which would you prefer a lesser note that allowed you to save money on the side to create an emergency fund, invest for retirement and handle all future financing needs (this is a biggie because it keeps you from incurring new debts!) OR a higher note that will keep you from saving anything, disallow an emergency fund, may propel you into new debts, but IF IT DOESN’T then you will be debt-free in half the time? Which would you choose?

It is at this point that the 15-year mortgagee throws out their last hoorah, “But I will be able to save my entire house note after I’ve paid it off!” That’s true, but rarely done since they are usually further in debt or not disciplined enough to start saving the note…and wasn’t the alleged point of the short-term mortgage the thrill of being “debt free” so you could spend all that money!

In any case, let’s compare the claims. So flash forward another 15 years. The 30-year mortgagee has continued to save his $456.47 per month, but now the 15-year mortgagee got serious and started saving $1,372.52 per month over that same time period. Both earned the same 5%. So what are the side funds worth for each person: $382,378.35 for the long-term borrower, $368,731.89 for the short-term borrower.

It is still true that the short-term borrower experienced less costs, around $70,000 less, but the pre-paying of those costs came at a price. And again, let’s pose the mortgage question in a different way and see which one you’d opt for:

Would you rather have:

- A 30-year note of $1,372.52 with an end value of $382,378.35? (The net effect of the 30-year mortgage); or

- A 30-year note of $1,372.52 with an end value of $368,731.89? (The net effect of the 15-year mortgage).

Now be honest!

But what is proposed to me repeatedly is option number “2” despite the poorer performance, the pitfalls along the way and the real world dilemmas that it presents. But that’s the power of bad financial information and the failure to address unintended consequences.

Finally, my experience tells me that the short-term borrower will never achieve even the value specified here ($368k) because they will end up in a cycle of debt that forever prevents them from “saving that house note” once the place is paid off. On the other hand, it is quite likely that the long-term borrower will both achieve this value ($382k) and exceed it because they have appreciated the value of cash flow, began regular savings early and, if they become their own banker, managed their debt for additional savings.