I do not hide the ball from my clients and prospective clients. I am more than straightforward with my advice about where to store their wealth since I even publish my recommendations. But there are dangers to being this overt and frank. One is the danger that my advice could be misconstrued or over-simplified. A second is that the recipient of the advice can become myopic, mistakenly focusing on pieces of the advice or recommended products, without having the experience necessary to appreciate the full strategy.

In such circumstances, I do not fault the advice-receiver. Everyone has to make their best decision based upon their own knowledge and judgments. Rather, I generally fault myself for not having the wisdom and aptitude necessary to effectively communicate a comprehensive message. It is a frustrating reality. I attempt to deal with this reality by adding additional advice to this blog. Perhaps by writing I can further express all the issues that a person would need to make the best, informed decision. That’s my hope at least.

Recently a prospective client, when considering whether to store his wealth in a life insurance contract, got sidetracked by two over-riding concerns:

- The cost associated with establishing a life insurance contract; and

- The idea that he could more efficiently “be his own banker” by storing his wealth in a bank account

I will say little about the first issue simply because ALL of the cost for setting up this program are generally re-captured within 3 to 7 years of initiating the plan (in the actual case it was less than 5 years) AND because much is added to a person’s financial health for those fully, reimbursed costs. Plus, I discussed those advantages in another blog.

Rather, I wanted to focus on the second issue: Whether one could achieve better returns and be more efficient by using a traditional bank product as the vehicle to “be your own banker” or whether the life insurance policy would prevail. I will spend the balance of this blog in doing so.

First, I have some experience with this. I have a client who has chosen to use a money market for his “bank” rather than a life insurance contract and my sense is that he has not done as well as the life insurance policy holders. That is purely anecdotal however, since I have not done the actual math to prove this out due to the impossibility of finding a proper point of comparison.

Still, it stands to reason based upon the very real difference between the condition of the two investors. To really “profit,” one has to be in the position of an owner of a company. For the life insurance policy owner in a mutual company, this is true. But for the account holder in a bank, not being in the position of an owner, they receive a payment only AFTER the owners have taken the profits of the company. That difference has a magnified effect as we apply the “self financing” principles of “being your own banker.”

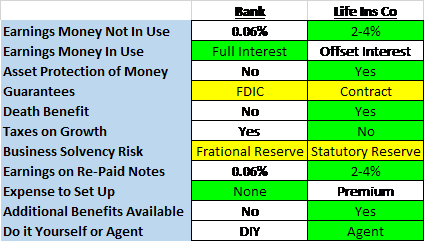

To illustrate this, I decided to draw up a little chart showing the differences between storing your money in a bank versus a life insurance contract. I added the future conditions of using the money via “self financing.” Here are my findings:

Clearly, the returns in the life insurance contract are better. This is true when the money is stagnant, which will probably be more often than not, and it is true as your money is repaid. The only time that the bank option shows a better return is when you are using the funds and that difference is smaller than might be imagined.

Clearly, the returns in the life insurance contract are better. This is true when the money is stagnant, which will probably be more often than not, and it is true as your money is repaid. The only time that the bank option shows a better return is when you are using the funds and that difference is smaller than might be imagined.

Add to this the fact that the life insurance policy is more tax-efficient, generally provides asset protection and gives a death benefit to boot and the case for using the bank grows smaller still.

All in all, the bank account holder only prevails in one category since the expenses to set up your life insurance plan, as stated before, are all recouped within a short period of time. One might claim a simpler, easier liquidity with the bank, but that is a double-edged sword. The delays of having to plan a “self financing” project and an agent to help you through the process will probably keep one from making many, costly mistakes.

Sometimes proof is not enough. Perhaps the reason for this is because proof is in the “now” and we often only find the truth through time and experience. Here’s to hoping that this proof will be sufficient to keep more people from losing their opportunity to really profit from “being their own banker.”

Hi, David.

I would add that the bank ROR isn’t keeping pace with the rate of inflation whereas the life contract is, so he’s actually back-pedaling .

In fact, he’s not even keeping the .6%. He’s keeping the net of his tax bracket and sharing a sliver with his partner at Internal Revenue, killing compounding unlike with the life contract.

For my money, the life insurance wins handily.

Best,

Kirk

Couldn’t agree more. That’s a great addition to the article. Thanks for the comment, Kirk!

David,

Thanks for this article. It just affirms what you have always told me but I couldn’t always envision. I keep putting you out there and hope to bring you more business in the future.

Bob:

As always, thanks for reading and for the positive comment. Helping folks like you is what brings us joy. And we appreciate the word of mouth advertising. Thanks for that too.

Hi David, any life policies you would recommend. I am 56 years old and would like to further investigate this

Silvio:

Please pardon this very late response. I have had someone working on my website and this comment was not forwarded to me. Yes, there are particular policies that you want to look for. I would be happy to help you find and build the right one. Why not email (david@tffco.com) to set up a time to discuss your options?

Hello David, I’ve listen to your program on the Crusade channel for several years. Would like to talk about setting up my bank of banking on myself.